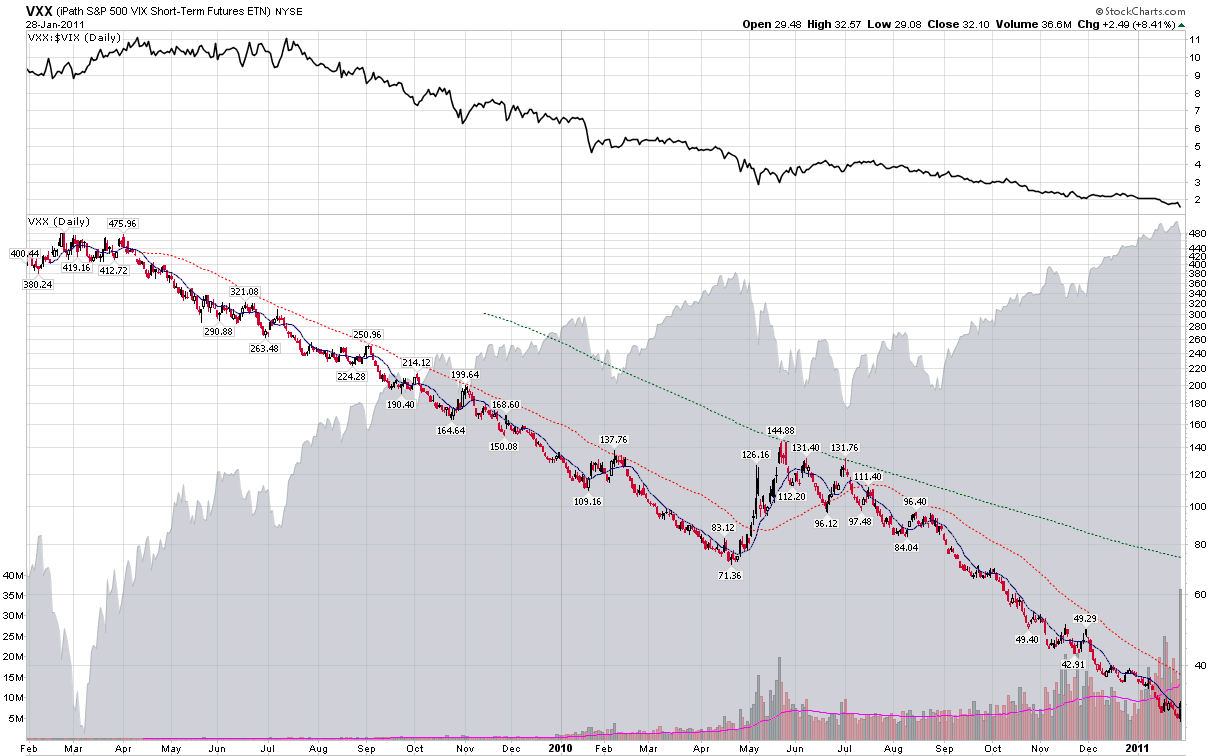

Chart of the Week: VXX Celebrates 2nd Birthday

Well, low bar or not, the performance of VXX was even worse in its second year than in its first year. In spite of the fact that VXX rallied 8.4% on Friday to close out the second year on a high note, its performance in the second year slipped to -74.6%, giving the ETN the dubious distinction of having fallen 92% since its launch two years ago.

While I have been chronicling the shortcomings of VXX for the better part of these past two years, let me go on record as saying that VXX does exactly what it sets out to do: capture a portfolio of VIX futures with a constant maturity of 30 days, with daily rolling used in order to achieve the constant maturity. As detailed in the links below and in many other places in this blog, it is the daily rolling in the face of persistent contango which triggers negative roll yield and acts as a drag on the price of VXX. In fact, VIX futures contango has been extremely elevated since the end of August, which largely explains why VXX lost 74.6% in the past year when the VIX declined only 18.6%. To compare the contango impact of the second year of VXX with the first year, all one needs to know is that in the first year VIX outperformed VXX by 26.2%, while in the year just concluded, VIX outperformed VXX by a whopping 56.0%.

This does not mean that investors should shun VIX as a volatility trade. In the short-term, VXX is a viable long volatility play, as evidenced by Friday’s 8.4% gain. When the VIX futures curve slides from contango to backwardation, VXX can also be an attractive trade. The problems on the long side begin when investors utilize holding periods of more than a couple of days. In the long run, volatility is mean-reverting and offers no natural directional advantage. For this reason, the longer the holding period, the more VXX trades become term structure rather than directional trades, with the term structure favoring contango over backwardation approximately 75% of the time.

With this in mind, I will repeat the same prediction I made one year ago, undaunted: VXX will perform better relative to the VIX in the coming year than it has in the past year.

Related posts:

- Why VXX Is Not a Good Short-Term or Long-Term Play

- VXX Calculations, VIX Futures and Time Decay

- VXX Monthly Performance

- Chart of the Week: VXX Celebrates One Year of Futility

- Chart of the Week: VXX vs. VIX

- Managing Risk with a Short VXX Position

- Charting the Assets of Volatility-Based ETPs

- VIX-Plosion 2011

Quite the green candle in VIX on Friday. After meandering for the week, VIX exploded 24% on Friday, the largest single day pop since those Flash Crash days of last May. What’s it all mean? Well of course, we won’t know until this plays out. But its not uncommon to see rushes for volatility like […]