The 10 year treasury yield is now 110 bps off its lows and where it stops nobody knows. It was my speculation that interest rates would increase, but the markets often move more abruptly than one expects. The ten year took over 5 months to drop from 3.5% to 2.4%, but it only took two months to retrace those steps.

Spiking due to government debts or backing away from a deflationary forecast?

The increase in yields could be attributed to:

- Fear of large US deficit and debt levels

- Better outlook for economic growth and inflation

- A lack of demand going into year-end

- Re-allocation of fixed income investments into equity markets

I personally dismiss number 2 because the unemployment report was rather sour and economic news has not pointed to an abundance of growth. Number 4 does not seem to hold a lot of water since the sell off in bonds has not been accompanied by a strong rally in equities and most of the rate movement occurred after the equity rally.

Number 1 holds a decent amount of weight considering the fact that Moody’s is threatening a ratings downgrade on the United States and because the movement in rates became more vicious after the hint of tax cut extensions and an Obama introduced reduction in the payroll Social Security tax of 2%. I did find an interesting comment which suggested that a temporary reduction in taxes increases the deficit, spurs short term consumer spending, but actually does little to boost the economy over the long-term because a short-term reduction does not give small businesses enough confidence to actually hire employees.

On a historically positive note, the yield curve is at record steepness levels:

The 30 Year 2 Year spread is at 3.87%!

At a spread of 3.87%, the steepness of the yield curve is at 30 year highs. This should be very stimulative as investors are not paid to sit on short-term investments, but paid to put money into riskier assets. As I have shown before, a steep yield curve can be a very positive signal for equities and therefore predict lower implied and realized volatility going forward.

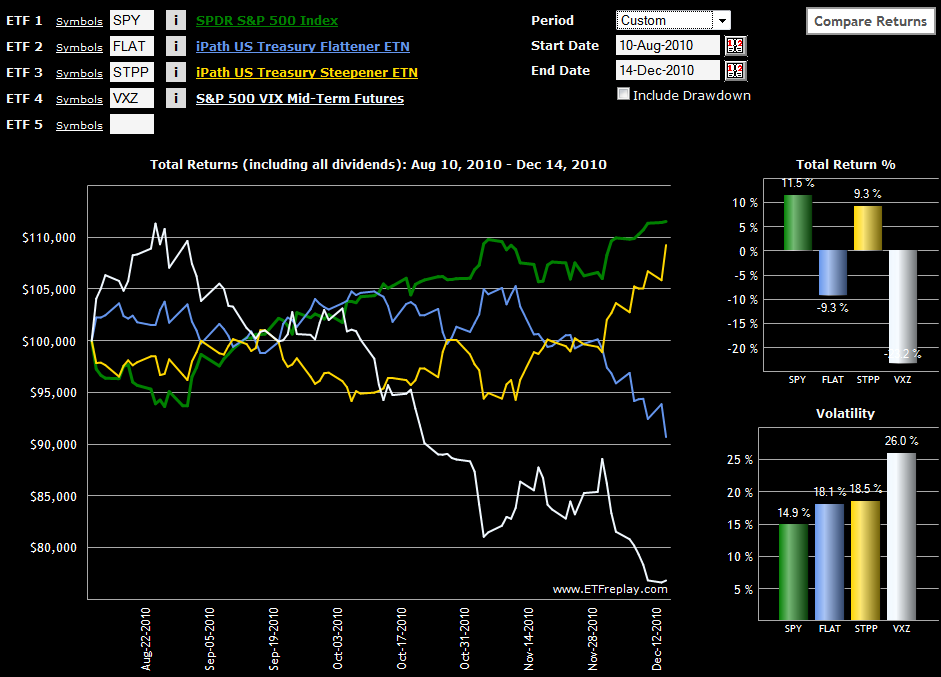

The more interesting trade idea is to look at yield curve flatteners. Yield curves cannot remain historically steep forever as you assume short rates would come up closer to long rates as growth is ignited and the Fed starts easing on the gas pedal. Obviously it is hard to predict when the growth will be ignited, but it seems that a 30 year historic high in yield curve steepness serves as a good entry point. The most direct way of placing this trade is to short two year bond futures and go long 10 or 30 year bond futures. This trade obviously requires access to a margin account with futures trading on the CBOT. As a simple alternative, the iPath Treasury Flattener ETN FLAT provides a nice prepackaged solution. Go long FLAT and you are shorting the two year and going long the 10 year without the hassle of a margin account.

A historically steep yield curve could provide a good opportunity to enter into a curve flattener

Even though I have been negative on bonds due to the previously low yields, I also am not overly bearish once the 30 year gets near 5%. We are still struggling with a sluggish economy and yields will have a natural cap as growth expectations are muted. Unless growth and a strong decrease in unemployment come out of left field, 10 year corporate bonds with 5.5 – 6% yields will look attractive compared to other investments.